When it comes to financing a purchase or managing your cash flow, understanding the different payment methods and their associated interest rates is essential. Whether you’re considering credit cards, personal loans, or other financial tools, it’s important to evaluate the potential impact on your financial health. Let’s delve into the common payment methods and how their respective interest rates compare.

Credit Cards

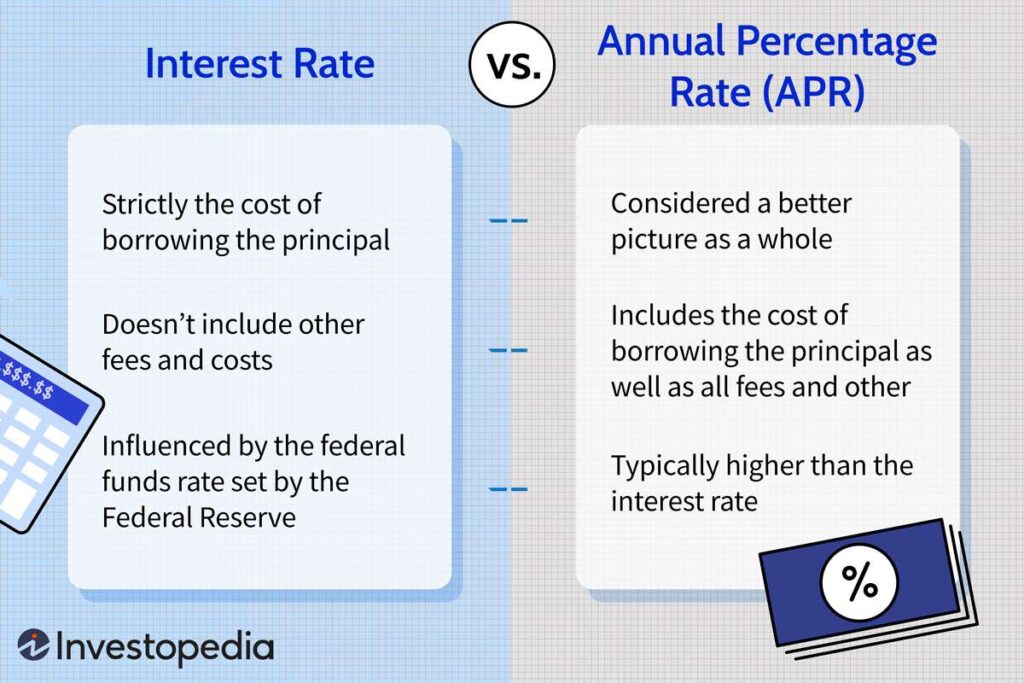

Credit cards are widely used for making purchases and managing everyday expenses. However, they are also known for carrying some of the highest interest rates among consumer financial products. The average credit card APR (Annual Percentage Rate) can range from 15% to 25%, and for individuals with lower credit scores, it can even surpass 25%. This high-interest rate makes credit card debt one of the most expensive forms of borrowing money.

Payday Loans

Payday loans are short-term, high-interest loans that are typically due on the borrower’s next payday. They often charge extremely high interest rates, sometimes reaching triple-digit APRs. While they can offer quick access to cash, the exorbitant interest rates associated with payday loans make them a very expensive form of borrowing, often trapping borrowers in cycles of debt.

Personal Loans

Personal loans, especially those categorized as “unsecured,” can also have high-interest rates. APRs for personal loans can range from 6% for individuals with excellent credit to over 36% for those with poor credit. It’s important to carefully consider the interest rate and terms of a personal loan before committing, as the higher rates can significantly increase the overall cost of borrowing.

Installment Loans

Installment loans, such as those for purchasing furniture or electronics, often come with high-interest rates compared to other financing options. While rates can vary depending on the lender and the borrower’s credit profile, they generally range between 10% and 30%. It’s important to compare offers from different lenders and consider the total cost of borrowing before committing to an installment loan.

Credit: www.forbes.com

:max_bytes(150000):strip_icc()/Lowerofcostandmarketmethod_final-cba5b199f508448280cdcc05d4f8ebc8.png)

Credit: www.investopedia.com

Merchant Cash Advances

For business owners in need of quick funds, merchant cash advances provide a way to access capital based on future credit card sales. While these advances offer convenience and speed, they also come with very high-factor rates, which translate to APRs that can exceed 100%. Business owners should carefully evaluate the cost of these advances and explore other financing options before committing to such high-interest rates.

Comparing Interest Rates

When comparing the interest rates of various payment methods, it’s clear that credit cards and payday loans typically carry the highest APRs. Personal loans and installment loans also often come with higher rates compared to secured loans like mortgages or auto loans. It’s important for consumers to assess their financial situation and explore lower-cost alternatives before choosing a payment method with high-interest rates.

Frequently Asked Questions On Which Payment Method Typically Charges The Highest Interest Rates: The Costly Truth

What Payment Method Typically Charges The Highest Interest Rates?

The payment method that typically charges the highest interest rates is credit cards. Credit cards often have higher interest rates compared to other payment methods.

Why Do Credit Cards Generally Have Higher Interest Rates?

Credit cards generally have higher interest rates because they are unsecured loans, meaning there is no collateral. This makes them riskier for lenders, which leads to higher interest rates.

Are There Any Payment Methods With Lower Interest Rates Than Credit Cards?

Yes, there are payment methods with lower interest rates than credit cards. For example, personal loans or lines of credit may have lower interest rates compared to credit cards.

How Can I Avoid High-interest Charges When Using Credit Cards?

To avoid high-interest charges when using credit cards, it is important to pay off the balance in full each month. By doing this, you can avoid accruing interest on your purchases.

Conclusion

In conclusion, the payment method that typically charges the highest interest rates is often the credit card, followed by payday loans and certain types of personal and installment loans. Understanding the interest rates associated with different payment methods can help individuals and businesses make informed decisions and avoid falling into costly debt traps. By comparing rates, reading the terms carefully, and exploring lower-cost options, borrowers can mitigate the impact of high-interest payments on their financial well-being.

Hopefully, with this information, you can make more informed decisions about the payment methods you choose.